Milk, Dairy and Grain Market Commentary

- Apr 24

- 4 min read

By Sarina Sharp, Daily Dairy Report

Milk & Dairy Markets

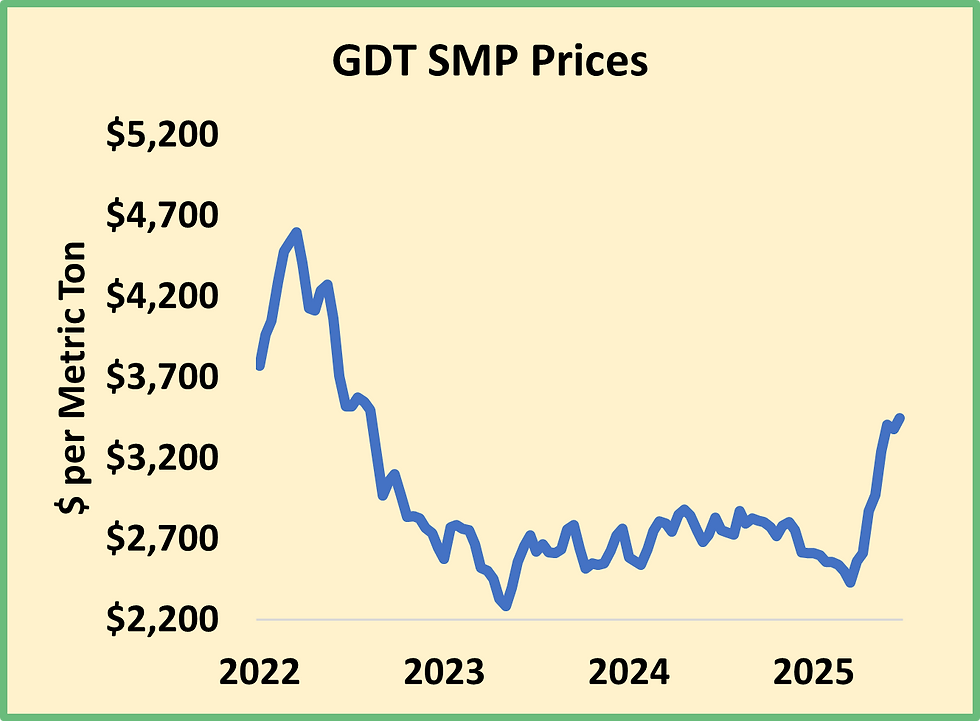

The short squeeze continues. Someone – or several someones – desperately need milk powder and they need it now. USDA’s Dairy Market News reports that prices are high enough that most milk powder users “are only buying loads to meet their immediate needs.” But for those that can’t do without, “it is difficult to find loads.” They bid the spot nonfat dry milk (NDM) market all the way up to $2.26 per pound this week, up 6ȼ from last Friday to a fresh all-time high. The spot market strength is spilling into other arenas. NDM futures rallied at the upper end of their daily trading limits several times this week. Skim milk powder prices reached a 3.5-year high at Tuesday’s Global Dairy Trade (GDT) auction. And LaSalle Street was barraged with traders looking to capitalize on the unusually wide spread between nearby Class III and Class IV prices. Today, May Class IV futures closed at $22.29 per cwt., a whopping $4.73 above May Class III. If both contracts settle in this realm, this will be the second-highest Class IV premium to Class III for any month in the past 15 years. Traders betting that the chasm would narrow bought Class III futures and sold Class IV, lifting the Class III market in the bargain.

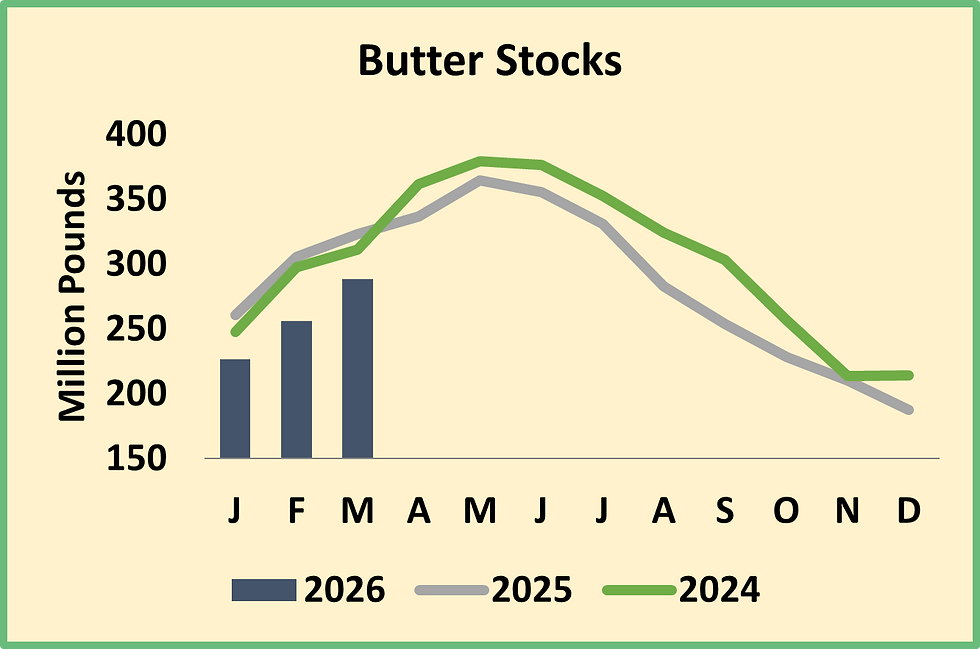

After much back-and-forth spot butter also gained some ground. It closed today at $1.705, up 1.5ȼ this week. But the spot market strength belies weakness elsewhere. Butter and anhydrous milkfat prices plummeted at this week’s GDT auction. May through September butter futures notched life-of-contract lows on Thursday. And USDA’s Cold Storage report, which was published after the closing bell, revealed a disconcerting jump in butter stocks in March. Inventories ballooned 33 million pounds last month, the largest February-to-March increase since 1991, at the height of the low-fat craze. Stocks are still 10.6% lower than they were the year before, but the deficit narrowed considerably from a 16.2% year-over-year shortfall in February. It seems that U.S. butterfat output is growing even faster than exports.

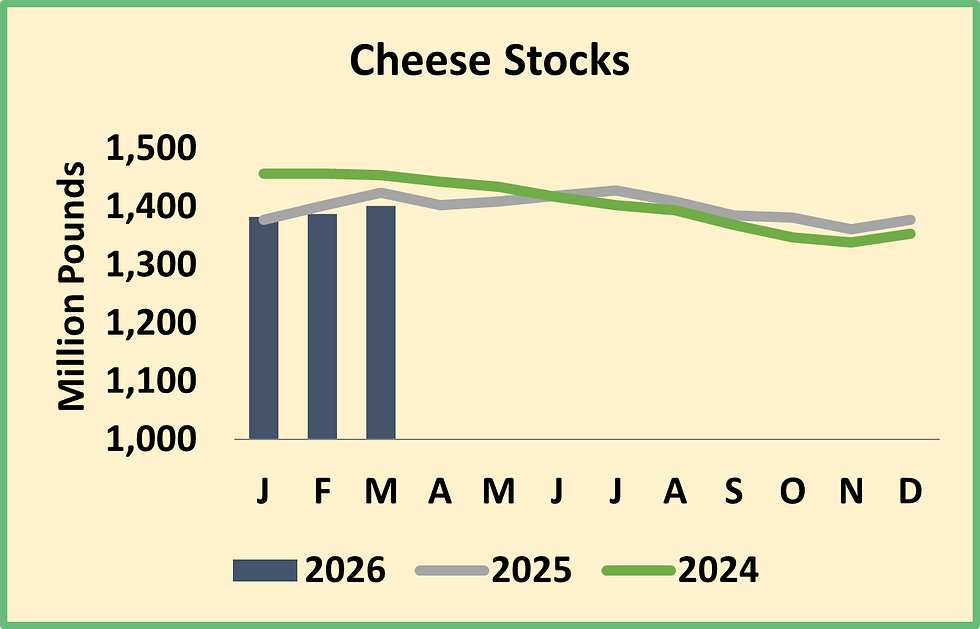

Cheese inventories climbed too, but the 13.5 million pound increase was in line with seasonal trends. Cheese output is formidable, but thanks to record-smashing exports and decent domestic demand, cheese stocks are not burdensome. March inventories were 1.6% lower than 2025 volumes and the lowest March tally since 2020. Relatively tight stocks buoyed Cheddar prices from their late-2025 and early-2026 lows south of $1.40/lb. This week, CME spot Cheddar blocks rallied 6.75ȼ to $1.645 per pound. But further upside may be limited. The U.S. dairy industry has invested in significant increases in cheese production capacity, and prices must stay low enough to maintain robust exports. Otherwise, cheese can pile up very quickly.

The whey market is hovering just below the 70ȼ mark. This week CME spot whey inched up 0.75ȼ to 69.75ȼ. Global demand for protein seems insatiable, and processors are maxing out production of whey protein isolates. But as Dairy Market News notes, “Cheesemakers are running busy production schedules, leaving plenty of whey for drying.” Thankfully, importers are looking to the U.S. for whey, and the market feels balanced.

With all spot products moving higher, milk futures jumped. May Class III rallied 56ȼ to $17.56. May and June Class IV added 85ȼ apiece and closed north of $22. The futures forecast summer prices in the $18s and $19s for Class III and into the $20s for Class IV. Coupled with record-smashing beef incomes, dairy producers have every incentive to expand.

And they continue to do so. Last month, producers added another 8,000 head, and the dairy herd expanded to 9.621 million cows, once again reaching the largest dairy herd since 1993. There are 187,000 more milk cows in U.S. dairy parlors than there were a year ago, and together they made 2.3% more milk than in March 2024. The industry expected big increases in cow numbers in the states that also boasted big expansions in processing capacity. And indeed, there are 47,000 more cows in Kansas than there were a year ago. The Texas dairy herd is up 31,000 head year over year, and dairy producers added 24,000 cows in New York, 18,000 cows in Idaho, and 15,000 cows in South Dakota. But the industry is also absorbing expansion in Wisconsin (+27,000 head) and Michigan (+16,000 head) where investments in processing capacity were slight in comparison. In contrast to growth in the Plains, where a few new massive dairies account for most of the increase, growth in the Great Lakes has been incremental, with a new heifer barn here and a parlor revamp there. We can expect more growth of this kind. The big push to add cows in the Central Plains is largely complete, but the market is screaming at producers to find ways to keep their barns and milk tanks full.

Grain Markets

Grain prices climbed this week as the market adjusts its risk assessment. Last year’s corn crop was massive, but exports have impressed. There’s still plenty of grain in the bin, but the trade now expects a little less of it by next harvest. That puts more pressure on this season’s corn crop. Farmers aren’t in a panic about fertilizer prices or the slow planting pace in the soggy eastern Corn Belt, but the market is pricing in a modest risk that either acres or yields will be impacted by these developments. And drought in the Plains has boosted wheat prices, given further support to the grain market bulls. There’s very little chance that U.S. grain supplies will be tight, but they may be less abundant than the market assumed a few months ago. With that in mind, July corn futures added 6.5ȼ this week and closed at $4.635 per bushel. But the soy complex sagged. July soybean meal futures fell $8 this week to $319 per ton.

This game is alright if you just want something simple to use in free time. I downloaded it few days back and till now everything worked normally. I liked that signup process didn’t take too long. App design is basic but clean enough. I don’t use it regularly every day because after sometime same feeling starts coming again and again. Still, for short use it keeps things interesting. Not perfect obviously, but I have seen worse apps too. Overall okay experience from my side till now.

BDG Game apk download