Copy of Milk, Dairy and Grain Market Commentary

- May 8

- 4 min read

By Monica Ganley, Quarterra

Milk & Dairy Markets

Nonfat dry milk (NDM) remains the belle of the dairy ball as prices rose to fresh record highs this week. On Thursday, the spot price hit an all-time peak of $2.295/lb. though the price dipped a half cent on the final day of trading. By the conclusion of Friday’s spot session, NDM was up 2.75¢ from last week. While elevated NDM price levels have provided an encouraging lift to Class IV milk prices, they have also made U.S. milk powder uncompetitive compared to other international suppliers and have severely limited the opportunity for U.S. manufacturers and traders to mint new export deals.

This challenge began to manifest in March as U.S. milk powder exports dipped 7.8% year over year during the month. U.S. suppliers shipped 59,522 metric tons (MT) (131.2 million pounds) of powder abroad in March, the lowest volume notched for the month since 2017. Exports to Mexico slipped by 6.8% year over year as buyers shied away from expensive product. Shipments to other key destinations in Southeast Asia and the Middle East also tumbled as importers sought more affordable sources for their needs. Given that high prices have persisted, U.S. exports of milk powder are expected to remain under pressure over the coming months.

Scarcity of product has been the key driver behind higher milk powder prices, and processors have taken note. In response to elevated price levels, combined production of NDM and skim milk powder rose 10% year over year in March with production hitting 212.7 million pounds for the month. While the increase relative to prior year levels is encouraging, milk powder production remains significantly lower than in recent years and supply constraints are likely to remain a factor in the market, even after today’s short squeeze has passed.

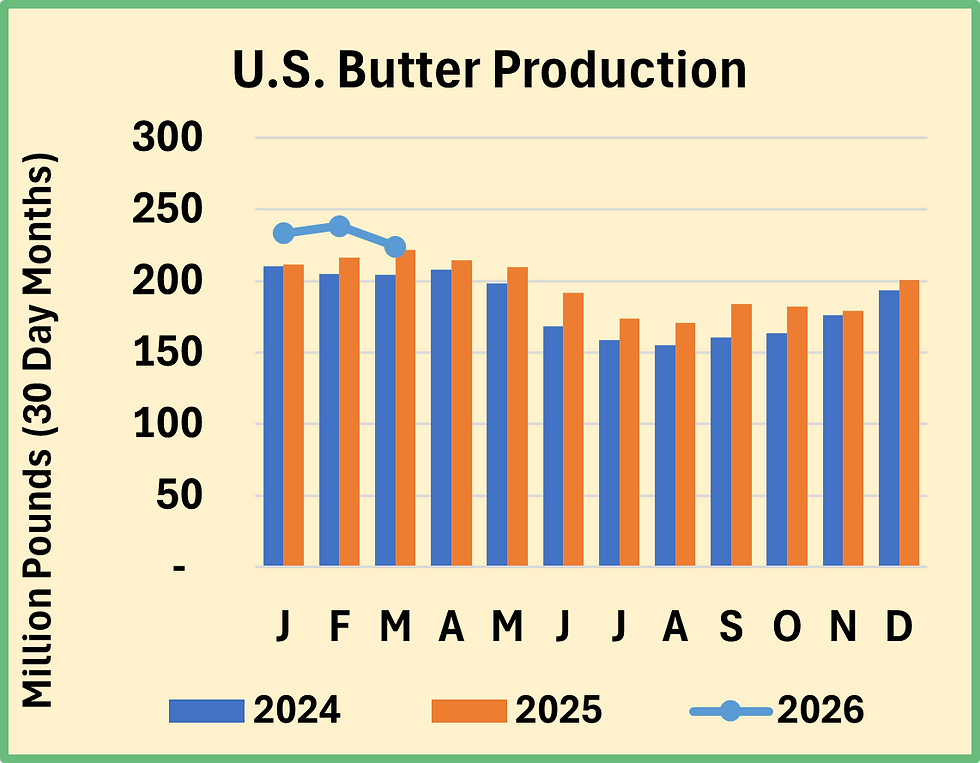

Though well shy of the lofty NDM values, butter prices also found some traction at the CME this week. Even as the price fell on Monday and Thursday, gains on the other trading days were sufficient to lift the price to $1.665/lb. by Friday. This delivered a 7¢ increase compared to last week as 38 loads of product traded hands. Cream remains plentiful and butter production is upbeat. USDA pegged March butter production at 231.5 million pounds in March, up 1.2% from prior year. Most of the volume was sourced from the western region where volumes were up 3.6%, though California production fell by 5% year over year.

The export market continued to provide an important outlet for U.S. milkfat in March as butterfat shipments were more than double prior year volumes. Butter exports were up 85.5% year over year at 11,337 MT (25 million pounds) while anhydrous milkfat saw shipments rise a whopping 184% to 5,737 MT. While U.S. butterfat remains competitively priced against other suppliers, continued geopolitical conflict could create mounting challenges in the coming months. Though March data continues to show an increase in butterfat volumes bound for the Middle East, it is unconfirmed if this product actually arrived at its destination. Future data releases will provide a clearer picture of the impact of the war on U.S. dairy exports.

Meanwhile, cheese exports continue to march ever higher, setting new records month after month. U.S. suppliers sent an eye watering 63,435 MT (139.9 million pounds) of cheese abroad in March, 28.7% more than the same month last year. A broad swath of destinations are contributing to the increase in cheese exports though notably, shipments to Mexico, South Korea, and Australia were up 40.2%, 78.9%, and 135.6%, respectively. With the global appetite for cheese unlikely to slow in the coming months, U.S. cheese exports are expected to remain upbeat over the balance of 2026.

Supply availability and price competitiveness have left the U.S. uniquely well positioned to meet rising global cheese demand. Cheese production was up 1.2% year over year in March with output totaling 1.258 billion pounds. Notably, however, performance was varied across geographies as Italian styles saw production rise 2.3% due especially to a 20% increase in Parmesan production. Meanwhile, output of American varieties slipped 2.3% versus last year, owing to a 2.0% decline in Cheddar production. Sufficient, if not excessive, supplies have kept prices trading comfortably in the $1.60s in recent weeks. Respecting these boundaries, the spot price for Cheddar blocks netted a 1.75¢ decline this week ending today’s spot session at $1.6225/lb. with 36 loads moving.

With cheese production buzzing there has been plenty of raw whey available. Manufacturers are gobbling up as much as possible to make high value ingredients such as whey protein isolate, production of which increased another 11.8% year over year in March. Raw whey which doesn’t make it into high protein production is routed toward the other end of the spectrum. While output of whey protein concentrates for human consumption fell 7.8% in March, production of dry whey for human consumption rose 8.5%. Despite stronger volumes, the dry whey spot price has remained stable, ending the week at 70¢ per pound, up a quarter cent from last Friday. A 37.1% increase in low protein whey export sales has likely kept prices supported. At the same time, U.S. exports of high protein whey products fell 31.8% in March, though the decline is likely due to intense competition with domestic sales rather than a slowdown in global demand.

Grain Markets

Grain markets moved lower over most of the week, owing to a few key pieces of market news. Importantly, lower oil prices contributed to bearish tendencies across the commodity complex, including for corn and soybeans. In addition, strong planting progress and weaker export sales have quelled supply concerns and led prices lower. Soybean traders, in particular, are anxiously awaiting next week’s summit between President Trump and Xi for clues about the future of the soybean trade between the U.S. and China.al producers.

Comments