Milk, Dairy and Grain Market Commentary

- May 22

- 4 min read

By Sarina Sharp, Daily Dairy Report

Milk & Dairy Markets

When Wile E. Coyote plummets off a cliff, Warner Brothers inevitably plays a “descending slide whistle.” That heart-dropping sound echoed across LaSalle Street this week as the bottom fell out of the milk powder market. The short squeeze is over. The two milk powder manufacturers who were desperately bidding for product to meet the commitments they could not fill with their own supplies due to food safety recalls have likely caught up and are back to using their own powder. And sky-high prices have killed demand from other buyers. Anecdotal reports suggest that Mexican milk powder buyers are turning to European suppliers who offer cheaper product even after adjusting for enormous differences in freight costs. Domestic buyers are in no rush to buy powder today if they afford to wait. The futures provide a steep discount to the spot market. Skim milk powder (SMP) prices inched upward at the Global Dairy Trade (GDT) auction on Tuesday, but, at the equivalent of $1.72 per pound, GDT SMP can stage a significant rally before it lends any strength to the U.S. nonfat dry milk (NDM) market. This week CME spot NDM plunged 20ȼ to $2.0725 per pound. If the selloff mirrors the depth and velocity of the rally, it could be a while before the descending slide whistle gives way to a splat.

But there is one bright on the horizon. After a long decline, Chinese whole milk powder (WMP) imports are on the rise. Thanks to a strong showing in March and April, Chinese WMP imports are up 6.3% for the year to date, their strongest four-month volumes since 2022. However, Chinese SMP imports in January through April are the weakest since 2015.

Chinese whey imports topped prior year volumes by 2.5% in April, and the U.S. accounted for nearly half the total. Decent exports and steady domestic demand have prevented a steep setback in the whey powder market. But output is on the rise. This week CME spot whey powder slipped a half-cent to 68ȼ.

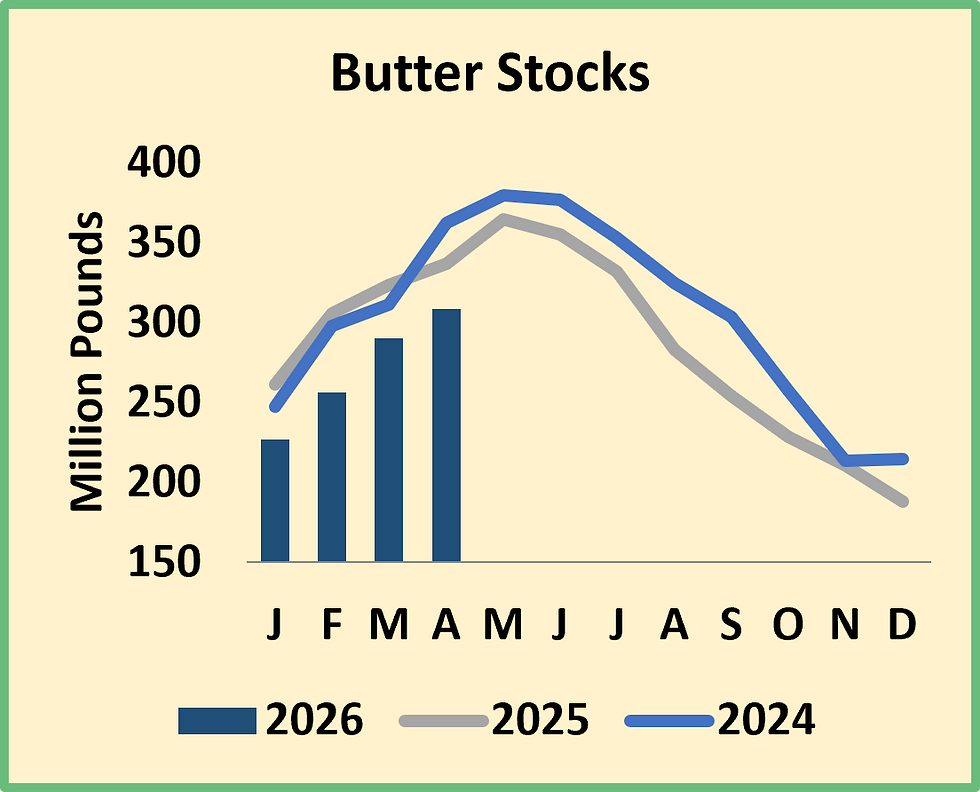

Butter prices dropped 10.5ȼ this week to $1.535, a four-month low. Stocks grew seasonally, but they remain 8.5% lower than April 2025 volumes. Butter production is robust, but exports are helping to keep supplies in check. Still, prices must remain low enough to maintain the current export sales pace.

CME spot Cheddar lost a nickel this week and retreated to $1.505. Cheese production is easily the strongest on record, and exports are strong too. Cheese inventories are 0.9% lower than they were a year ago. But American-style cheeses, including the Cheddar that helps determine Class III prices, are starting to pileup. Cheese stocks grew 12.4 million pounds from March to April, and American-style cheeses accounted for nearly the entire uptick. The steep increase in American-style cheese stocks in both March and April suggests that international buyers are not all that interested in U.S. Cheddar. If American-style cheese stocks continue to grow, some will wind up in Chicago and weigh on the CME spot price.

With lots of red ink in the butter and powder markets, Class IV futures nosedived. Most contracts lost $1 or more. June Class IV closed at $21.17 per cwt., down $1.33 for the week. Class III futures lost between 30ȼ and 97ȼ. That pushed the May through July contracts into the $16s, while August and September slumped to the mid-$17s. Still, dairy producers can expect to remain profitable thanks to decent milk prices and record-setting beef incomes.

Prosperity on the farm continues to add up to more milk. Dairy producers added 10,000 cows in April, and the dairy herd grew to 9.645 million head, the highest headcount since July through September 1993. There are 190,000 more cows than there were in April 2025, and milk yields improved 0.7% from a year ago. With that, milk output jumped 2.7% in April, matching March’s year-on-year growth and outpacing analysts’ expectations. The industry is now building on last year’s strength. The U.S. milk-cow herd had largely recovered from avian influenza by April 2025, and milk output that month was 1.8% greater than in April 2024.

Nearly every major dairy state contributed to the expansion. Dairy producers in Kansas cranked out 94 million pounds more milk than last year, a 23.7% increase. Top-ranked dairy states California and Wisconsin both made 79 million pounds more milk than in April 2025, while Texas added 67 million pounds of milk and Idaho’s and Michigan’s output jumped 45 and 42 million pounds, respectively.

Cattle prices plummeted this week. Nearby feeder cattle futures – which determine the price of dairy-beef cross calves – dropped more than $15 per cwt. from their mid-week peak. The beef industry remains chronically short of young livestock, but these calf prices simply don’t pencil. Calf buyers are growing increasingly wary of stocking their feedyards with livestock that project negative margins. It’s possible that crossbred calves and dairy cull cows have topped, but even if they suffer a significant drop, beef calf and cull cow revenues will still be higher than the checks that made dairy producers very happy just a few years ago.

Grain Markets

The grain markets took back some of the ground they lost last week. July corn rallied 9ȼ to $4.6375 per bushel. July soybeans jumped 20ȼ to $11.9725. After a big rally last week, July soybean meal slipped $2 to $332 per ton. As of Sunday evening, farmers had planted 76% of the corn crop and 67% of intended soybean acreage. Both figures are well ahead of the five-year average and should alleviate any concerns about lost acreage due to unfavorable spring weather.

U.S. corn remains competitive internationally, and exports are booming. American soybeans, on the other hand, look terribly overpriced to international buyers. South American supplies are plentiful and considerably less expensive. This week the Buenos Aires Cereals Exchange raised its estimate of the Argentine soy crop by 3.1% compared to last month’s projection. The prospect of yet another massive South American harvest should keep a lid on U.S. feed markets.

Comments