Milk, Dairy and Grain Market Commentary

- Apr 17

- 4 min read

By Sarina Sharp, Daily Dairy Report

Milk & Dairy Markets

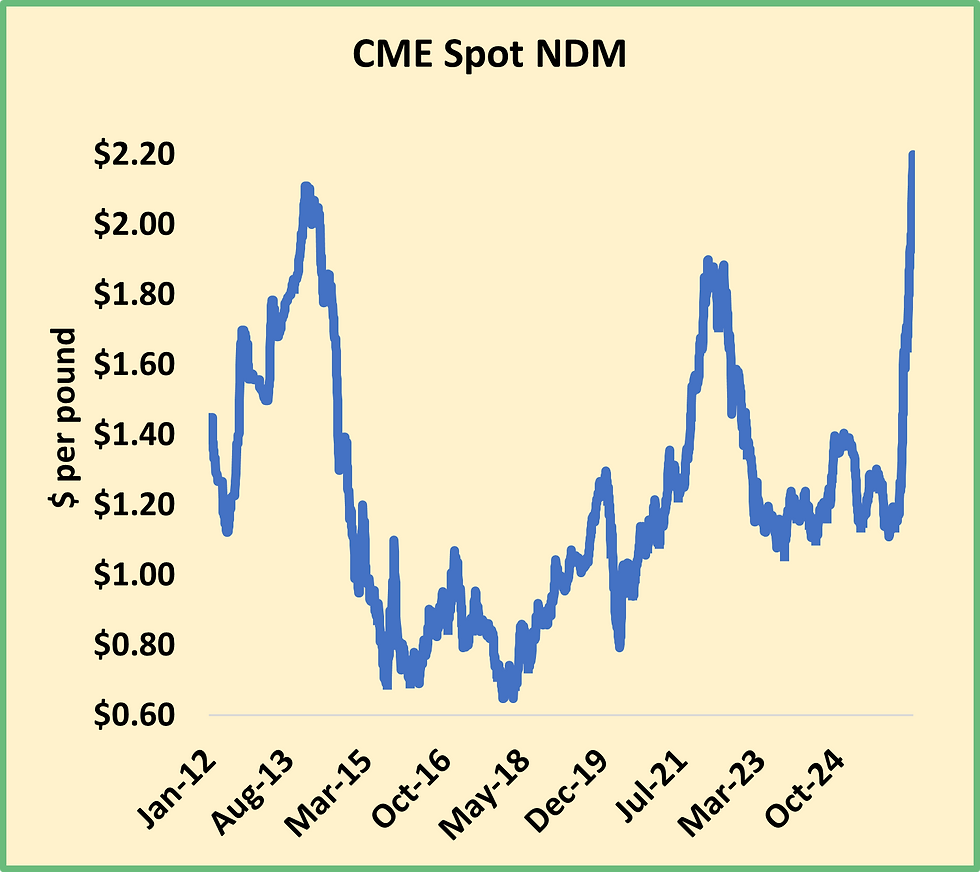

The milk powder market is sprinting straight uphill. Nonfat dry milk (NDM) rallied another 8.5ȼ this week and reached $2.20 per pound, the highest-ever price in the product’s 18-year tenure at the CME spot market. The short squeeze continues. USDA’s Dairy Market News reports that spot loads are tight from coast to coast, and they’re “particularly difficult to find in the Central region” where the expansion in cheese processing capacity has reduced the need for balancing. Even as milk production ramps up for spring, dryers in the region are running somewhat light.

But in California, milk is abundant, and dryers are running as hard as possible. As the spring flush overwhelms processing capacity, a major California cooperative is incentivizing producers to rein in milk output with steep discounts on any milk shipped above their monthly base volume. Last year, avian influenza dragged down California milk output and national NDM and skim milk powder (SMP) production slumped to a 12-year low. The California comeback matters. Last year, despite the bird flu, the Golden State accounted for 44% of U.S. NDM output. Now that California’s cows are healthy and happy again, production is up. U.S. milk powder output topped 2024 and 2025 volumes in January and February.

According to USDA’s Dairy Market News, domestic demand is strengthening, and exporters continue to ship product to Mexico. But other foreign buyers are looking elsewhere for their milk powder. And they should. U.S. NDM typically trades a little below SMP from Europe or Oceania. Today, it is about 60ȼ higher than international benchmarks. That chasm is wide enough that our competitors across the ocean might start selling to our next-door neighbors, which would surely shock the market. Mexico typically consumes about one-third of U.S. milk powder production. U.S. milk powder exports to Mexico topped year-ago volumes in January, but February shipments south of the border fell to the lowest tally for the month since 2022.

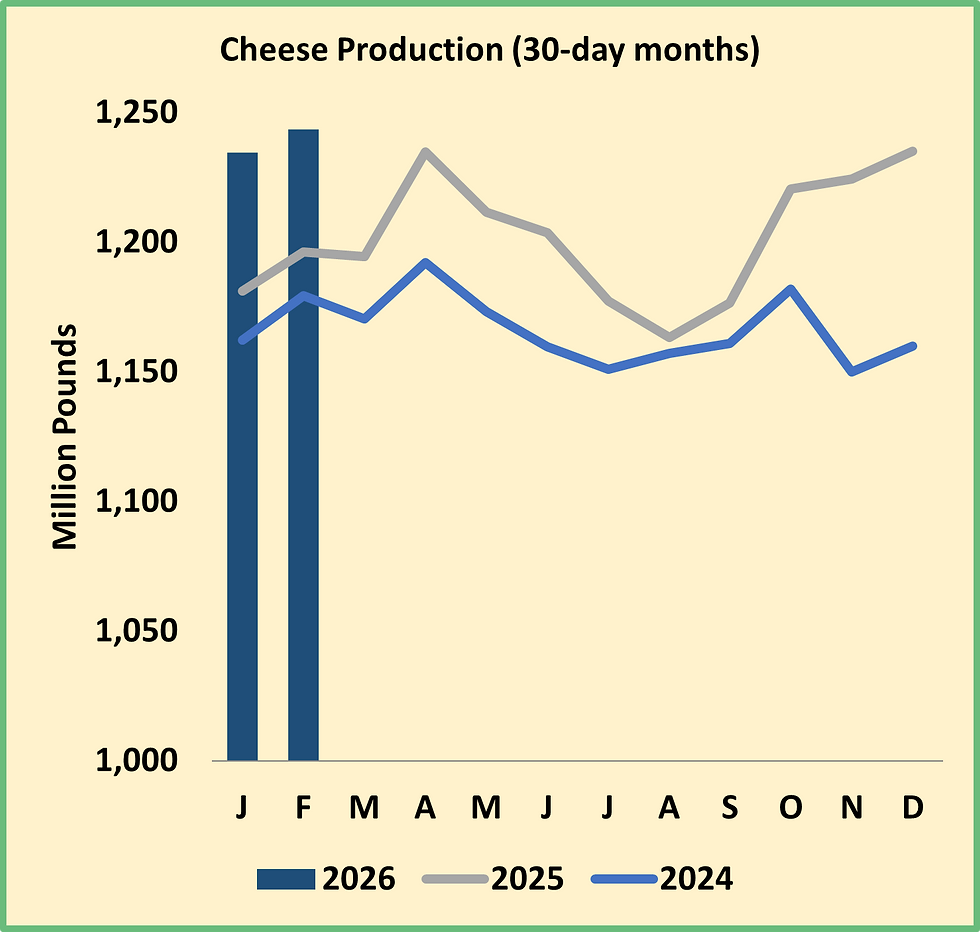

The other dairy markets showed none of NDM’s exuberance. CME spot Cheddar blocks and barrels both finished the week right where they began it, with blocks at $1.5775, in the middle of the recent trading range. This relative stability reflects a market that is concerned about record-shattering output but buoyed by record-smashing exports. The trends look comforting at first glance. In February, cheese output outpaced prior-year volumes by 3.9%, while exports set a new all-time high, with shipments up 30.1% from February 2025. But the absolute numbers are less reassuring. While output was 44 million pounds greater than the prior year, exports grew 32 million pounds. In January and February, exports absorbed just 43% of the year-over-year increase in cheese production. U.S. cheese prices must stay low enough to attract international buyers at the current breakneck pace. At some point, they may need to drop low enough to move cheese abroad even faster.

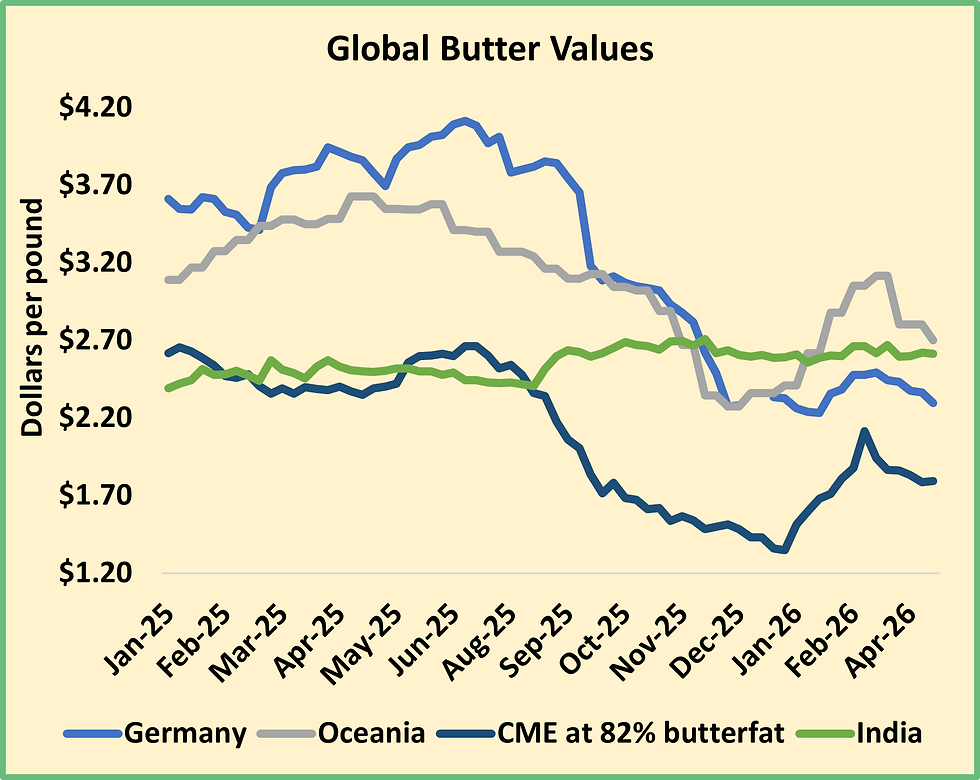

The U.S. butter market is also sensitive to cues from overseas. In January and February, butter production topped prior-year volumes by a combined 41 million pounds, while exports jumped 29.4 million pounds. U.S. butter maintains a decent discount below international prices, but to preserve it, Chicago futures must match international declines step for step. At this week’s GDT Pulse auction, both butter and anhydrous milkfat values dropped. CME spot butter fell 5.75ȼ to a two-month low.

Whey powder production is inching upward as greater cheese production translates – inevitably – into a greater whey stream. Manufacturers are making every high-protein whey product possible, and those continue to sell in huge volumes at phenomenal prices. But as manufacturers bump into capacity constraints on high-protein concentrates and isolates, there is plenty of whey leftover to make commodity powder. Whey powder production for human consumption topped the prior year in every month since May. Thankfully, exports are running hot and prices are holding close to the 70ȼ mark, providing great returns for dairy producers. This week, CME spot whey powder slipped 1.5ȼ to 69ȼ.

Milk futures were mixed this week, but most Class III contracts finished a little lower than last Friday’s settlement, while most Class IV contracts finished higher. The futures predict that April Class III milk will bring $16.85 per cwt., but the market calls for $19 Class III milk by September. For Class IV, the futures predict $20 milk in April and July, with milk futures above $21 in May and June. Dairy producers will also continue to cash huge checks as they sell cull cows and milk calves. Margins are excellent and expansion continues.

Grain Markets

Over the past six weeks the corn market followed the oil market up and then back down. July corn closed today at $4.57 per bushel, not far from where it stood in early March, when Iran shut down the Strait of Hormuz and constrict global oil flows. July soybeans closed at $11.815. In late February and early March, summer soybean futures hovered around $11.80. But there is one crop market that looks quite different. July wheat futures closed at $5.98 per bushel, 10ȼ to 15ȼ higher than where they stood in early March. Over the past two months, the Plains winter wheat crop has suffered drought, wildfires, and frost threats. Yields and quality have deteriorated.

LaSalle Street is also trying to determine the impact of higher fertilizer prices on farmers’ planting decisions, and whether some farmers will use fewer inputs and risk lower yields. This analyst believes the planting mix might change slightly on the fringes. But in the heart of the Corn Belt, farmers are likely to stick with their planned rotations. And the impact of the spike in fertilizer prices will be blunted by the calendar. A recent American Farm Bureau Federation survey found that two-thirds of farmers in the Midwest had purchased this year’s seed and fertilizer before the war began. The weather might have a greater impact on farmers’ planting decisions. Planters are rolling in the southern and western Corn Belt. But the states surrounding the Great Lakes have been pummeled by rain storms and there are more on the way. The fields are soggy and planters are parked.

Comments