Milk, Dairy and Grain Market Commentary

- Sep 1, 2023

- 4 min read

By Sarina Sharp, Daily Dairy Report

Milk, Dairy & Grain Markets

Cows in the Midwest got a brief break from the heat, but the mercury is going to climb once again over the holiday weekend. Midwestern dairy producers report that milk yields dropped hard last week and then recovered. They’re bracing for the next heat wave. Temperatures are projected to run 15˚ to 25˚ above normal in the Northern Plains starting today, with sweaty conditions moving eastward over the next few days.

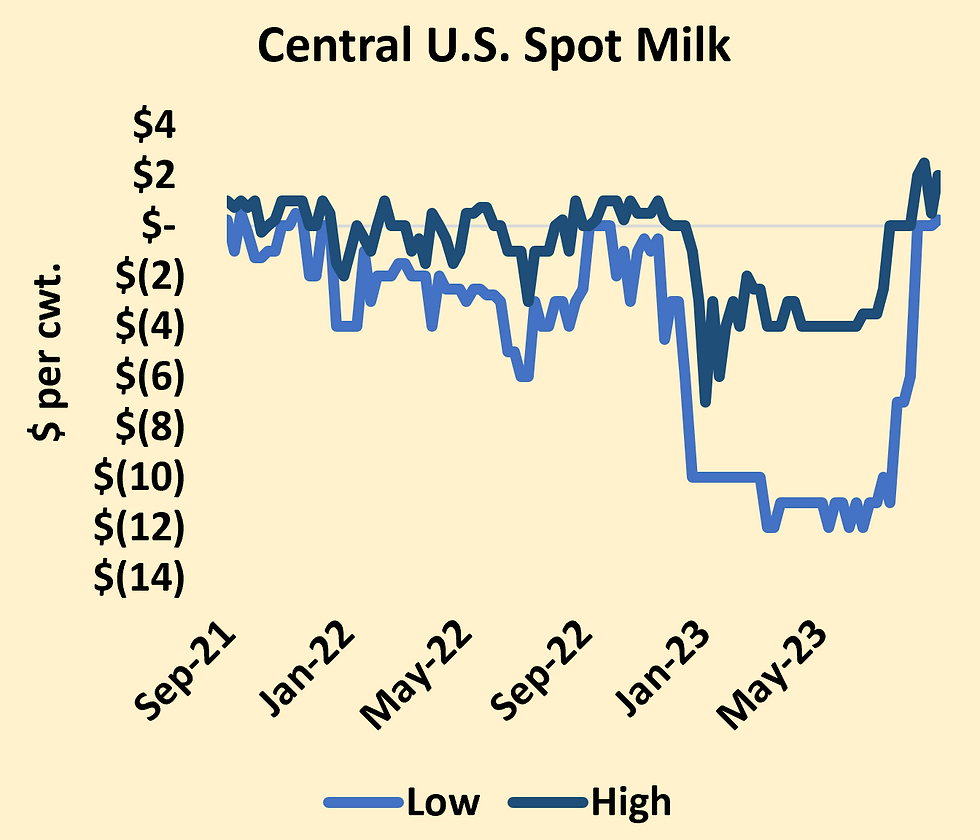

The combination of high temperatures and high cull rates have noticeably reduced milk supplies in the region. Despite anticipated slowdowns in dairy processing ahead of Labor Day, there was very little spot milk to be had this week. For the first time since 2021, every load of spot milk changed hands at a premium this week. Midwestern cheesemakers kept their vats full of cheap milk through the spring and most of the summer, but now they are slowing down. USDA’s Dairy Market News reports that persistent labor issues and an increase in bottling for school milk programs has slowed the flow of milk to cheese vats in the Northeast. Meanwhile, cheese output continues apace in the West.

Domestic cheese demand remains strong. The trade assumes that exporters are shipping cheese they committed to sell months ago, when prices were much lower. But fresh demand for exports is soft. Cheese prices perked up in Chicago, led by a 7ȼ jump for Cheddar barrels. They closed today at $1.87 per pound, matching their highest price since March. Blocks stepped boldly toward the $2 mark and then backed away, but they still managed to gain a half-cent this week. They finished at $1.95.

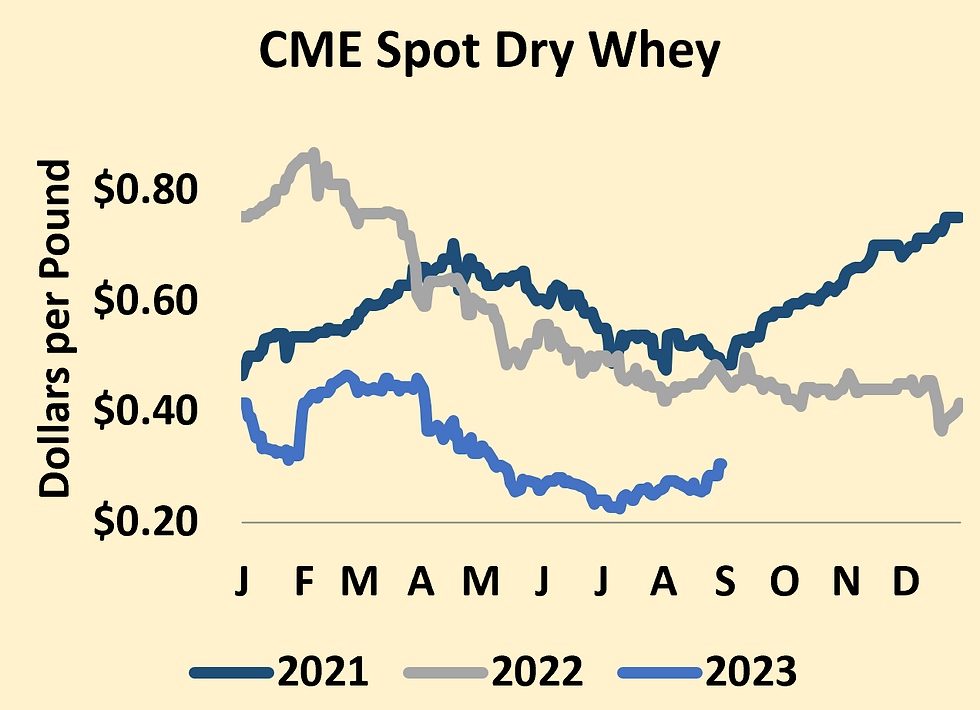

Slower cheese output has tightened up whey supplies and, at long last, demand for whey protein products is perking up. Manufacturers are shifting more of the whey stream into concentrates, leaving less for the drier. Dairy Market News summed it up last week, “Limited milk availability for cheese processing, along with recently firming high protein blend markets, have created a slightly bullish safety net for a market that has been struggling to gain traction for a better part of the calendar year.” CME spot dry whey climbed 2.5ȼ this week to 30.5ȼ, its highest mark since May. Dairy producers should be relieved to see some signs of life in a market that has been a drag on Class III values for so long.

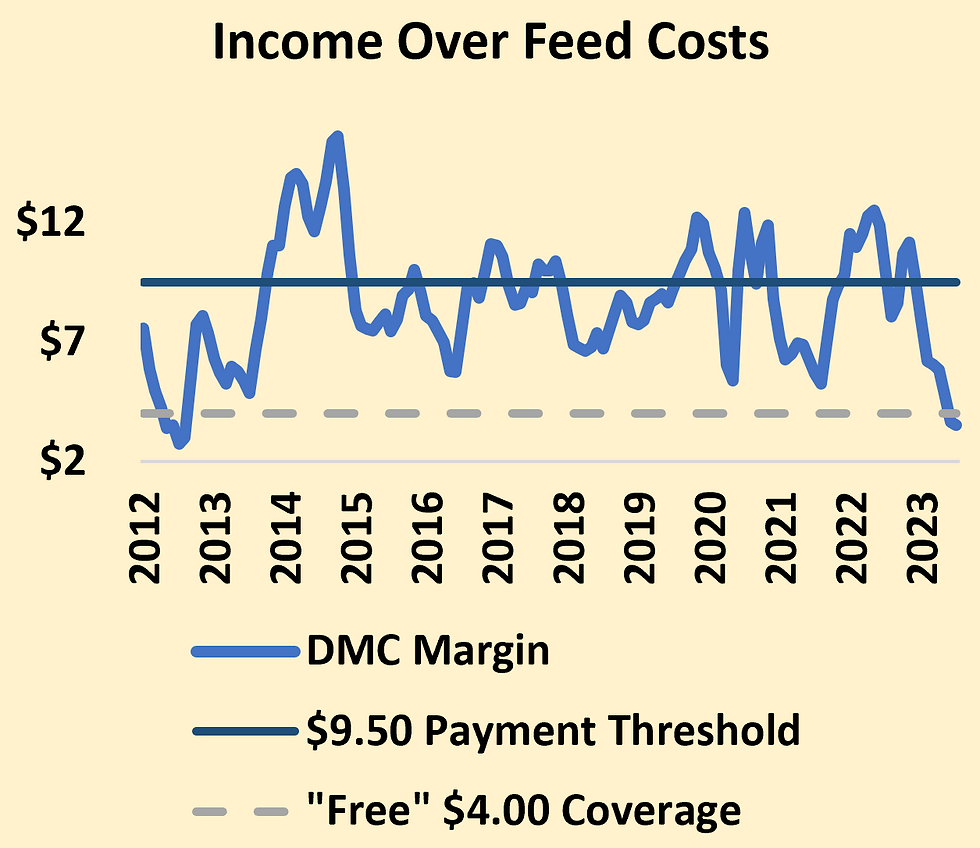

USDA announced the August Class III milk price at $17.19 per cwt., up $3.42 from a horrendously low $13.77 in July but down $2.91 from August 2022. The July milk prices pushed income-over-feed margins to just $3.52 per cwt. of milk production, according to the Dairy Margin Coverage (DMC) program’s formula, the lowest showing for the index since 2012. Dairy producers with 5 million pounds of annual DMC coverage at the highest – and most popular - $9.50 tier should expect indemnity payments of nearly $25,000 in both June and July.

Going forward, prices look much better, but, as the Daily Dairy Report points out, “With milk prices hovering between $18 and $19, some dairy producers will continue to lose ground, while others only inch forward on the long road to financial recovery.” September Class III futures closed at $18.63 today, down 31ȼ from last week’s exuberant close. Advances in spot cheese and whey prices helped all other Class III contracts to gain a little ground. The October contract jumped 28ȼ to $18.93.

USDA announced the August Class IV price at $18.91, up 65ȼ from July but still $5.90 lower than August 2022. Class IV futures retreated this week, with most 2023 contracts settling 40 to 50ȼ in the red. September Class IV settled at $18.50.

CME spot butter slipped a penny to $2.66. Despite the heat, cream multiples are in decline, and butter makers are ramping up output. Ice cream production is winding down and, now that bottlers are working harder to satisfy school milk demand, they have more cream to sell. Demand remains strong. In the first half of the year, domestic butter consumption reached a new high, up 8.7% from the first six months of 2022.

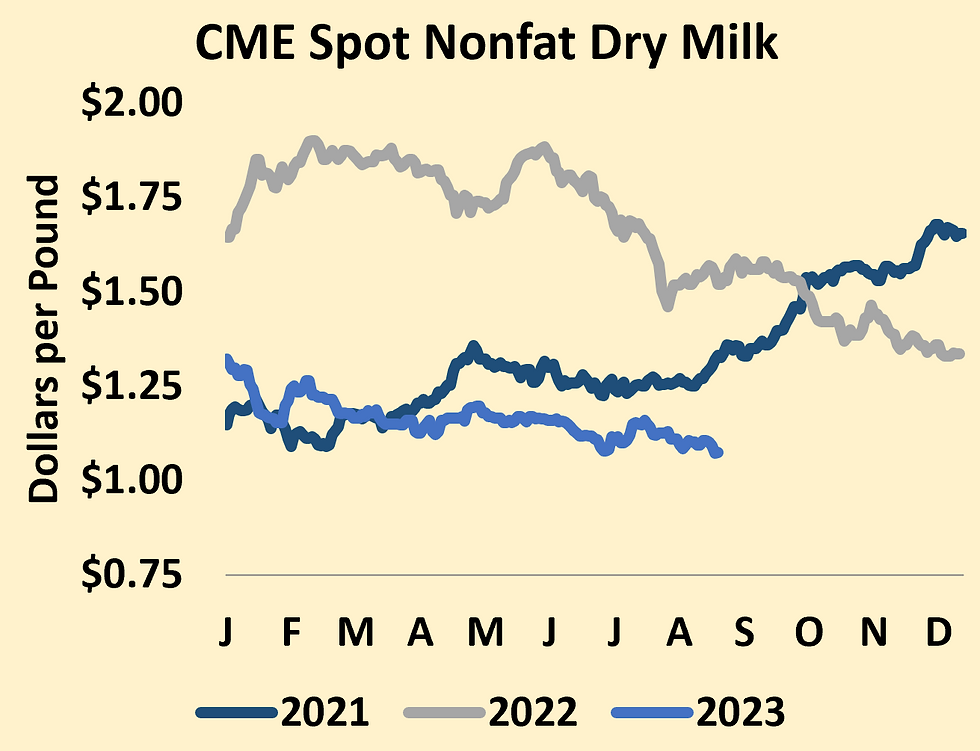

Milk powder prices fell once again. CME spot nonfat dry milk (NDM) dropped 3ȼ to $1.075, a new 2023 low. Tighter milk supplies have reduced drying activity from coast to coast. Dairy Market News reports that in California, “some balancing plants are not currently operating.” Nonetheless, milk powder prices just can’t get up off the mat. Supplies are fading, but demand continues to disappoint. Until Chinese whole milk powder imports improve, Kiwi and European merchants will sell milk powder at prices low enough to keep product moving. Closer to home, some cheesemakers are starting to fortify their vats with NDM now that spot milk has dried up. There are hints that low prices may finally be starting to cure low prices in the U.S. milk powder market.

Grain Markets

Feed values retreated. December corn closed today at $4.815 per bushel, down 6.5ȼ from last Friday. November beans fell 18.5ȼ to $13.6925. December soybean meal dropped $15.40 to $399.60 per ton. Much of the setback came Tuesday, on the heels of USDA’s weekly assessment of crop conditions. The agency reported modest declines in corn and soybean ratings, but the trade had expected worse after last week’s sky-high temperatures. The trade will be watching closely to see how the crops fare after what promises to be a scorching long weekend. Corn kernels and soy pods are drying quickly, which is likely to reduce yields as harvest nears.

Comments