Milk, Dairy and Grain Market Commentary

- Sep 12, 2025

- 4 min read

By Sarina Sharp, Daily Dairy Report

Milk & Dairy Markets

There were no bulls to be found on LaSalle Street this week. The bears roamed freely, showing no fear of an overcorrection even as parts of the dairy complex scored multi-year lows. Red ink poured into the cheese and milk powder trade and deluged the butter market. CME spot butter plummeted to $1.86 per pound, down 16.25ȼ in just five trading sessions. Spot butter is down more than 40% from the mid-summer high, languishing at its lowest level since October 2021, nearly four years ago. The weakness carried across the futures board, with May through October 2026 contracts dropping 10ȼ or more on Friday. Milk production is strong and cream is plentiful and cheap. Churns are running hard. Exports for both butter and anhydrous milkfat are booming, but they’re still not high enough to lap up all the excess cream.

There’s plenty of milk for cheese as well. CME spot Cheddar blocks fell 7.5ȼ this week to $1.615, just a few cents above their year-to-date low. USDA characterizes export demand as “steady” which is good news considering the record-high export volumes achieved this summer. But domestic demand is also on par with summer levels, which were not so hot. Restaurants continue to use less cheese than they did in 2024 even as U.S. cheese processors make more. That’s a recipe for lower prices.

U.S. milk powder output is not heavy. Even so, demand is not keeping pace. Domestic consumption is slipping, and the U.S. is not winning a lot of export business outside Mexico. Global milk powder demand is in the doldrums, and international prices are slipping. Global Dairy Trade skim milk powder (SMP) and whole milk powder (WMP) values dropped hard at least week’s auction, and they retreated further at this week’s Pulse event. European SMP prices also waned even as USDA described European SMP output as “lighter.”

European milk powder production could climb in the months to come. Europe’s dairy industry weathered a hot summer and threats of bluetongue and lumpy skin disease and still managed to expand output. Milk collections in the EU-27 outpaced the prior year by 1.2% in July. British milk output easily lapped year-ago volumes, and when British collections are added to the mix, regional milk production was 1.6% greater than it was in July 2024. That’s a marked departure from earlier this year, when milk output hewed close to 2024 volumes and often fell short. The world seems unprepared to absorb simultaneous – and significant – growth in European, American, and Kiwi milk output, especially as economic data points to darker days ahead.

Once again, the whey market bucked the trend. CME spot whey powder rallied 2.75ȼ this week to 59.25ȼ. USDA’s Dairy Market News sums up the market well. “Cheesemakers continue to run busy production schedules, leaving plenty of liquid whey available for drying, but plant managers say much of this is going towards higher whey protein concentrates. Dry whey production remains limited overall, though stakeholders say production is trending higher.”

Unfortunately, the whey complex is not strong enough to support milk prices all on its own. Most Class III contracts lost between 25 and 60ȼ this week. October Class III settled at $16.31 per cwt., a life-of-contract low. Class IV futures fared even worse. October Class IV plunged $1.13 to $15.90. Traders offered to sell Class IV milk south of $16 per cwt. all the way into February, while deferred futures slumped to the mid-$16s. Feed costs are low and beef revenues are unbelievably high, but many producers will struggle to make ends meet with $15 and $16 milk.

Grain Markets

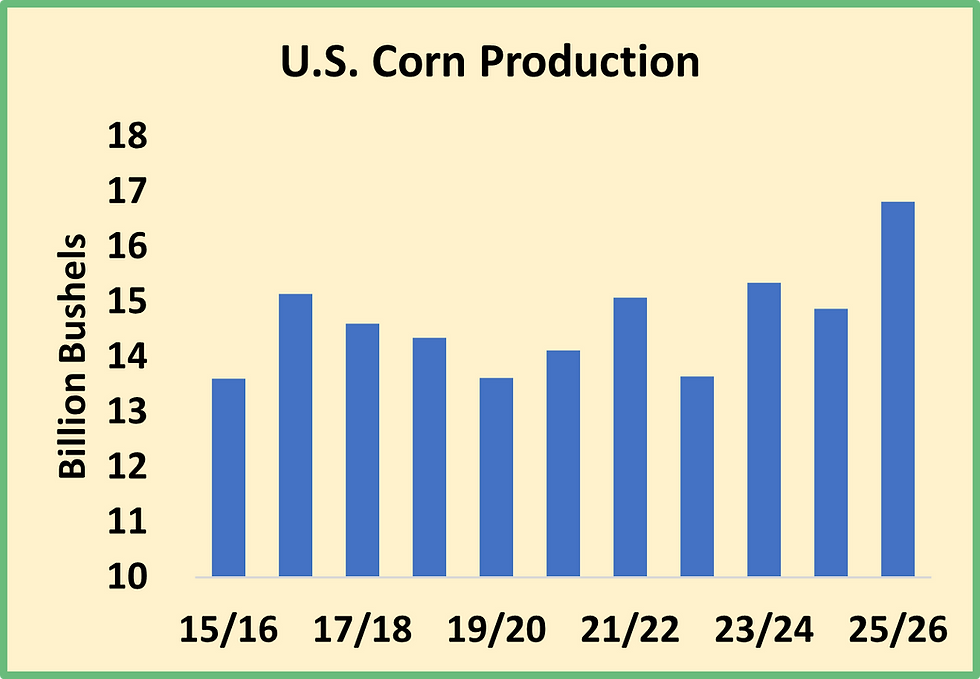

As expected, USDA trimmed its estimates of national average corn and soybean yields from the very high figures posited in August. The agency pegged the corn yield at 186.7 bushels per acre, down from a forecast of 188.8 bushels last month. If the final yield is anywhere close to this number, farmers will harvest their largest crop ever. For soybeans, USDA now expects the crop to average 53.5 bushels per acre, down slightly from the August estimate of 53.6 bushels per acre.

But USDA also raised its assessment of corn and soybean acreage. The agency raised corn planted area to 98.7 million acres, the highest total since 1936. The increase in acreage more than offset the decline in yields, and USDA now projects that farmers will harvest 16.8 billion bushels of corn, 72 million bushels more than they expected in August. That’s 10% more grain corn than the previous record-large harvest of 2023. That means even more corn available to be shipped abroad, so USDA raised its export forecast to a record-high 2.975 billion bushels.

A modest increase in soybean acreage had the same effect, putting USDA’s latest production estimate of 4.3 billion bushels slightly ahead of the August prediction of 4.29 billion bushels. With that, USDA expects that there will be 2.11 billion bushels of corn and 300 million bushels of soybeans leftover at the end of the 2025-26 season. Abundant crops will keep dairy producers’ feed costs in check for the next year and possibly beyond. But prices may have fallen low enough to spark new demand. Despite the bearish report, both corn and soybean futures rallied Friday afternoon. December corn settled at $4.28 per bushel, up a dime for the week. November soybeans closed at $10.45, nearly 20ȼ higher than last Friday. December soybean meal closed at $288.20 per ton, up nearly $5.

Comments