Milk, Dairy and Grain Market Commentary

- May 17, 2024

- 3 min read

By Sarina Sharp, Daily Dairy Report

Milk, Dairy & Grain Markets

The bulls ran wild in Chicago this week. For both Class III and Class IV milk, June through December futures notched life-of-contract highs. Dairy producers are cashing a pitiful April milk check but looking forward to much more prosperous times ahead. The May Class III contract closed at $18.73 per cwt. and June climbed 93ȼ this week to an astounding $21.47. Most Class IV contracts finished about 50ȼ higher than where they began the week.

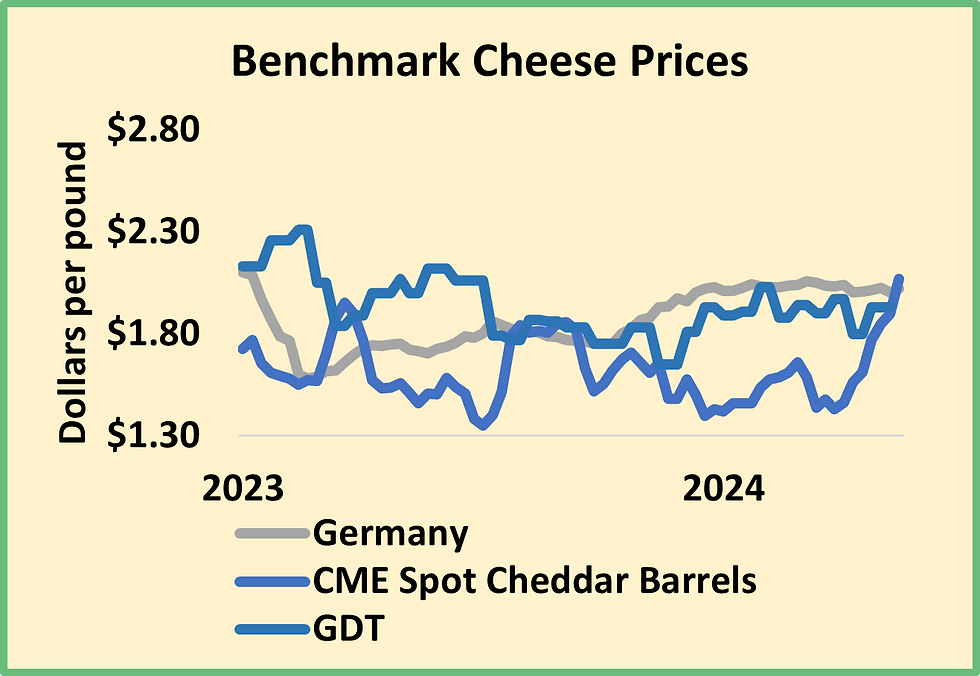

The barrel market led the charge. CME spot Cheddar barrels soared 21.25ȼ this week to $2.125 per pound, their highest price since October 2022. Blocks faded after nearing the $2 mark and closed at $1.9425, down 3.75ȼ. Slow Cheddar output and booming exports tightened cheese supplies in the first quarter. Localized milk shortages and maintenance downtime continue to restrict output of fresh barrels ready for delivery to the Chicago spot market. Although these high prices should encourage an uptick in cheese production, shortages of fresh cheese are quite possible in the hot summer months.

USDA’s Dairy Market News reports that retail demand for cheese is “elevated” and that “Cheddar and Italian-style cheesemakers say they are turning down new orders.” But U.S. cheese prices are increasingly out of step with the global market. The export boom that fueled this rally could turn into a bust if foreign buyers back away from pricey U.S. cheese.

The butter market remains impervious to outside pressures. Production and inventories are higher than they were in the previous two years, and the U.S. continues to import butterfat. But buyers remain anxious, and they continue to bid enthusiastically. This week they exchanged 20 loads at the CME spot market and pushed prices back up to $3.07 per pound, 8ȼ higher than last Friday. September butter futures traded as high as $3.21. Consumers are undeterred. USDA notes that retail butter demand ranges “from steady to strong,” and foodservice demand is holding firm.

The powders also climbed. CME spot dry whey rallied 3ȼ to 41.5ȼ, a two-month high. High-protein whey stocks are tight, but commodity whey inventories are not, and exports continue to disappoint, so additional gains will likely depend on slower output. CME spot nonfat dry milk (NDM) also notched a two-month high, climbing 1.25ȼ to $1.165. Mexican buyers are increasingly interested in U.S. NDM, according to Dairy Market News, which has given the market a boost. U.S. milk powder output is already well below year-ago levels, and the deficit is expected to widen as milk tightens seasonally. Higher cheese prices and scarce spot milk could also push some cheesemakers to fortify their vats with condensed skim or NDM, cutting deeper into milk powder inventories.

The markets are clearly communicating that milk is tight, and dairy producers are listening. But with heifers in short supply, it’s difficult – and expensive – to fill every stall and top off the bulk tank. To take advantage of these much higher milk prices, it appears that dairy producers are slowing cull rates from already low levels. In the week ending May 4, producers sent just 48,975 cows to beef packers, the first time since June 2016 that slaughter volumes fell below 50,000 head in a non-holiday week. If the herd expands, it will certainly help to boost milk supplies, but the impact will be muted by the fact that, in order to boost head counts, producers are keeping some lower-production milk cows in the herd for longer than they have in the past. In other words, milk yields likely won’t climb as quickly as they once did.

Some of our competitors are already boosting milk output. Assuming steady production trends in Spain, which has yet to report, milk output in the EU-27 and United Kingdom topped 31 billion pounds in March, up 0.5% from the year before. Australian milk collections were up 4.4% from the prior year in March. However, in New Zealand, fluid milk collections fell 3.5% year-over-year in March, and milk solids output slipped 1.2% below prior-year levels.

Grain Markets

The grain markets took a step back this week. Once again, wheat futures led the way, and corn followed. The trade remains concerned about weather issues around the globe – and especially dry weather in Russia and flooding in southern Brazil – that will trim harvests. Certainly, global grain and oilseed production appears smaller than it did a few months ago, but it is still expected to be historically large, and old-crop stocks are ample. With that in mind, July corn fell 17ȼ to $4.5275 per bushel. July soybean meal closed at $368.80 per ton, down $3.70.

Comments